Cyber and technology risk has moved to the centre of private equity value creation, and the larger funds have built real capability around it. The question for a mid-cap fund is not whether it can match that capability pound for pound - it is how to reach the same confidence by a route that suits its economics. There is one, and it is well within reach.

Two routes to the same confidence

Private equity is deliberately careful about accountability. A fund influences its portfolio companies from outside the operational boundary; the company remains the accountable entity. How much a fund can shape what happens depends on the holding. Where it holds a majority, it can instruct - mandate standards, protocols and reporting through its governance rights. Where it holds a minority, it can encourage - set expectations and make the case through influence. Either way, the fund sets the expectation and watches the result rather than running the function itself.

Large funds can afford to support that role with permanent infrastructure: operating partners, value-creation teams, and sometimes a dedicated security executive setting portfolio-wide standards and overseeing them across assets. It is an effective model, and an expensive one. Research from Russell Reynolds finds the leading firms increasingly treat cyber maturity not as protection but as a measurable, competitive strength they can benchmark and scale across a portfolio.

Mid-cap funds can apply an alternative approach that reaches a comparable result at materially lower cost. In our experience, rather than carrying permanent capability, the fund draws on it proportionately - enough to set a clear standard, maintain a current view across the portfolio, and act when something needs attention. The objective is identical; the cost base is not. This is the route worth understanding, because it is both achievable and efficient.

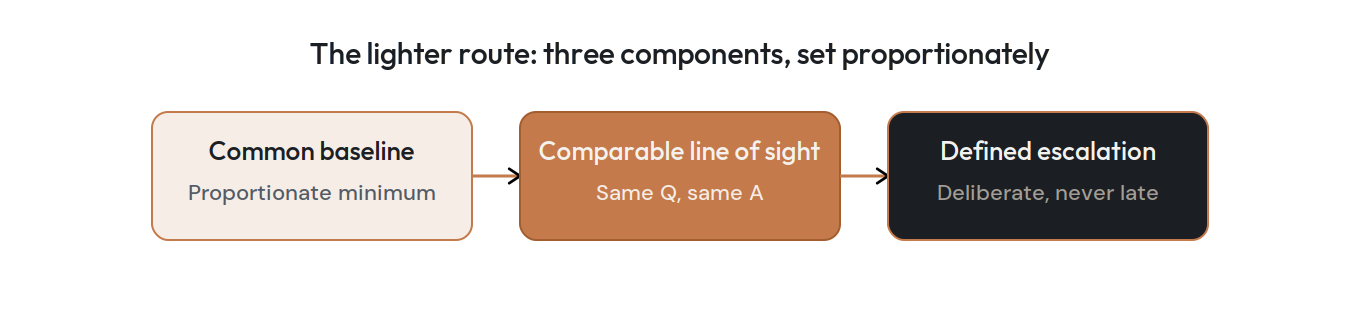

What the lighter route delivers

The approach rests on three straightforward components, set proportionately and kept current.

A common, proportionate baseline. A clear minimum standard - asset visibility, privileged access, backup and recovery, tested incident response - expected of every portfolio company and scaled to the size and complexity of the asset, rather than a one-size framework imposed uniformly. The fund sets the expectation; the company owns the execution. Instruct where the holding allows it, encourage where it does not.

A comparable line of sight. A consistent, light reporting rhythm that lets the fund see across the portfolio which assets meet the baseline, which are on a plan, and which would benefit from attention. The value is in comparability - the same questions, answered the same way - so the fund can weigh one asset against another with confidence.

A defined escalation path. When an asset would benefit from intervention, a known route brings it to the fund’s attention promptly and deliberately. Nothing is left to chance or discovered late.

None of this asks the fund to take operational control, and none of it requires a permanent team. It gives the fund what it actually wants: a clear standard, a true view, and the ability to act - held precisely to the level of accountability the fund is comfortable carrying.

Why it matters most at exit

This approach earns its keep throughout the hold period, in lower duplicated spend and a steadier risk position. It pays off most visibly at exit - and the shape of today’s market is what makes it matter. Deal and exit values recovered through 2025, but the easy returns did not come back with them. Bain’s read on the current era is that low prices, cheap debt and easy multiple expansion are gone, that “12 is the new 5” in the EBITDA growth deals now demand, and that the path to value creation has to be articulated and evidenced from day one. Returns now come from operational quality, not financial engineering. A fund cannot control the macro backdrop. It can control how well its asset stands up to scrutiny.

That is where cyber and technology posture becomes a lever rather than a liability. Bain urges funds to look past the headline deal case to an asset’s full potential, scrutinising the revenue, operational and technology levers that drive a step-change in performance - and disciplined buyers now do exactly the same in reverse. Unresolved technology risk is a known way to lose value at the table. As AlixPartners observes from the buyer’s side, nothing scares an acquirer quite like the prospect of a long, high-risk transformation - an unfinished ERP migration is precisely the kind of open-ended commitment that gives a buyer pause and pulls down the price. A fund that has kept a clear, evidenced view of its assets meets that diligence with answers already in hand, and negotiates from a position of equal or better knowledge of its own company.

The upside is well evidenced. In EY’s 2025 study of private equity exit readiness, the large majority of firms reported that exit-preparation work improved their valuations to some degree. Preparation is one of the few exit variables a fund genuinely controls, and cyber and technology readiness is a part of it that is too often left until the diligence questions arrive. The lighter route does not simply reduce cost and risk during the hold; it converts cyber and technology posture from a question raised in diligence into a point of confidence the seller can stand behind.

A practical first step

The entry point is modest: a single diagnostic across the portfolio that establishes which assets are well controlled, which would benefit from attention, and where the quick wins are. From that baseline the fund gains a comparable view within a quarter, places any assets that need work on a manageable track, and sets the reporting rhythm before the next deal cycle - so each new acquisition joins a system that already exists.

It is a small, proportionate investment that compounds: lower duplicated cost across the portfolio, a steadier risk position through the hold, and a stronger hand at exit in a market that now pays for demonstrable operational quality. For a mid-cap fund, that is an efficient way to turn cyber and technology from an open question into a managed advantage.

The same discipline now faces its next test. AI is a genuine source of value when it is applied diligently, and a source of cost and risk when it is driven by hype or panic. The funds that will benefit are the ones whose portfolios approach AI the way they should approach cyber - deliberately, evidenced, and on their own terms. That is the subject of the pieces to follow.

SOURCES

Bain & Company, Global Private Equity Report 2026 (February 2026)

Russell Reynolds Associates, Creating Value with Cyber Security: What Leading PE Firms Are Getting Right (November 2025)

AlixPartners, Lessons learned in maximising the valuation of portfolio companies on exit (October 2024)

EY, Private Equity Exit Readiness Study 2025 (2025)